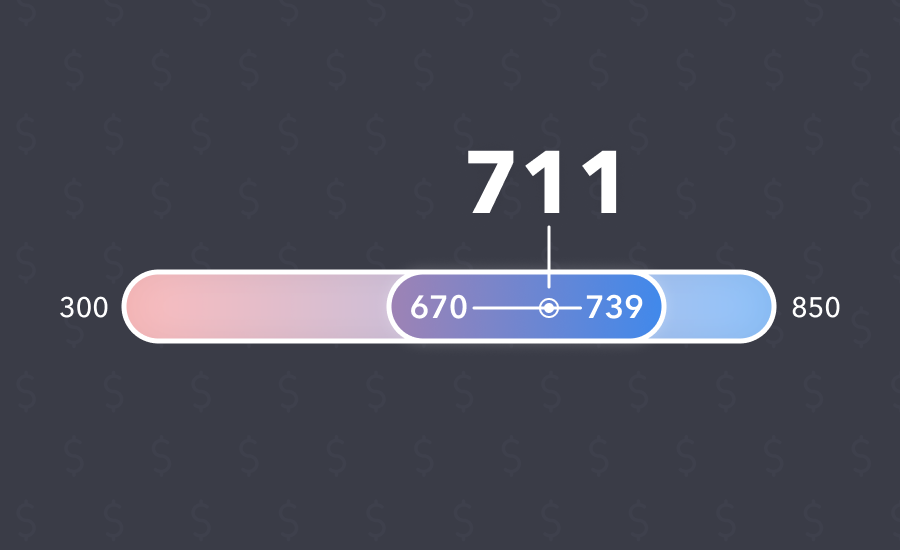

Credit scores for the average American continue to climb. In 2019, the average U.S. FICO score was 703. Last year, the average was a record-setting 711.

At first glance, this is good news. As most consumers know, FICO and other credit scores are important litmus tests for lenders considering loans. The higher the credit score, the greater the likelihood of low-interest rates, increased borrowing power and more. Conversely, poor credit scores usually mean higher interest rates. Or, they may mean no loan at all.

But that’s not all. Many employers consult credit scores when determining a person’s eligibility to work. Landlords, too, refer to them when weighing pondering prospective tenants.

In other words, even though credit scores offer only a narrow glimpse into someone’s overall financial health, they carry a lot of weight. And just one oversight by a consumer – a tardy or forgotten bill payment, for instance – can badly tarnish an otherwise solid credit history.

The Low Down on Credit Scores

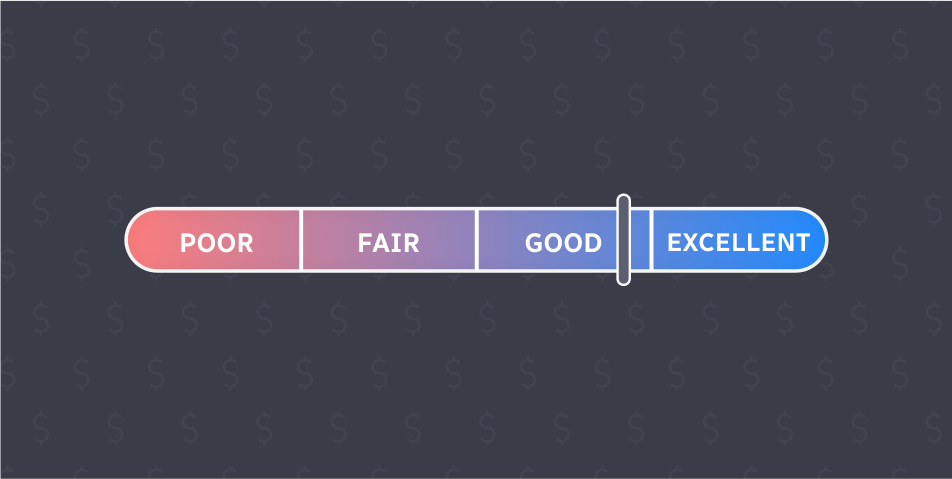

FICO scores range from 300 (“very poor”) to 850 (“exceptional”) – with “poor”, “fair”, “good” and “very good” falling in between those extremes. Most Americans score between 670 and 739, which places them squarely in the “good” category. So, even though 711 marks a new historical-high, most U.S. consumers qualify only as good credit risks.

It may sound like hair-splitting, but these distinctions have real-world effects. A 2020 LendingTree study determined a borrower classified as fair would likely pay more than $7,000 in interest over the life of a $25,000 auto loan versus a borrower deemed to be very good. That fair borrower would also likely pay significantly more in interest on all personal loans, student loans and credit cards.

Bottom line: credit scores play a crucial role in shaping how much access a consumer has to the financial mainstream.

Yet, for millions of Americans, that access is uncertain. Nearly one-third of U.S. consumers are classified as fair and very poor credit risks, and what may be surprising is how thin the cushion separating a good credit risk from a fair or even a very poor. It’s so thin, in fact, according to FICO that - depending on a person’s credit history - a single late bill payment “can cause as much as a 180-point drop” to a consumer’s credit score.

Meaning a consumer with a good score could overlook a bill and find themselves reclassified as very poor.

And this isn’t a prospect facing those with already-shaky credit histories. Just the opposite. The stronger a consumer’s credit history, the louder the alarm bells can ring if a payment is late. That’s because, in the eyes of lenders, the more stellar the credit history, the more troubling a missed payment.

Better Bill Pay Can Help

According to BillGO’s research, Americans pay more than 15 billion bills each year, which works out to be about a dozen bills a month for most Americans. That’s a dozen opportunities to overlook a payment and unintentionally damage a credit score.

But it doesn’t have to be this way.

In the world of retail payments, consumers have access to countless modern, convenient and frictionless methods to meet their financial obligations. But when it comes to managing and paying bills, the average consumer has far fewer options.

Yes, most financial institutions (FI) provide their customers with some form of bill payment technology, but the majority of those tools are out of step with the needs of today’s consumers, as demonstrated by the fact only 22 percent of consumers use them. Instead, 76 percent of consumers pay their online bills directly to biller websites, which is both cumbersome and risky when there are a dozen bills to juggle each month.

This is why BillGO is pioneering a more modernized method of paying and managing bills and subscriptions. Our award-winning, real-time bill management & payments platform puts consumers in charge of their financial obligations. They can decide when and how they pay their bills. They also have end-to-end visibility - from notifications that bills are pending to real-life confirmations showing payments have been made.

BillGO is driven by the belief that everyone deserves access to a healthy financial future. And, in the current landscape - where just one late payment can jeopardize a person’s financial standing - it’s essential consumers have the modern tools they need to fully manage their financial lives.

Next Steps

If you’re a consumer looking for a more efficient way to manage and pay your bills, ask your preferred financial services provider if BillGO powers their bill pay solution.

If you are a payments executive ready to give your customers with the modern tools they need to fully manage their bills, download a complimentary copy of BillGO’s eBook, How Financial Institutions Can Win the Bill Payment Game.